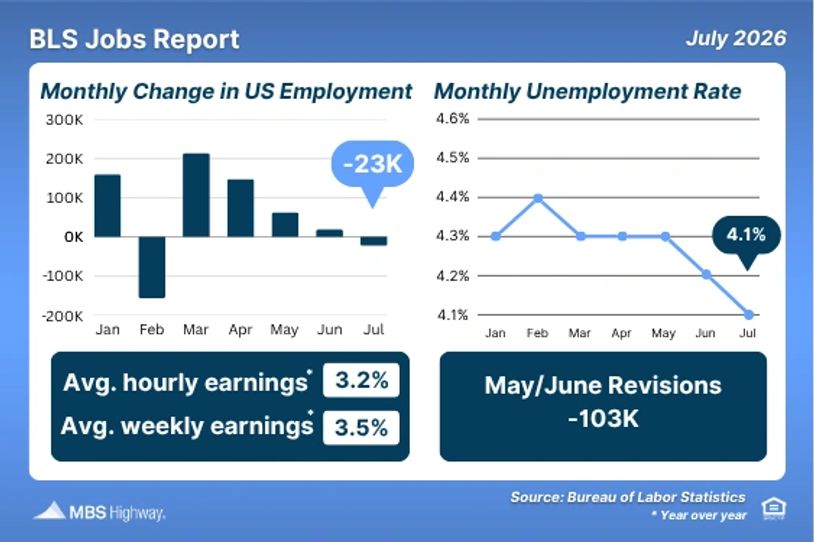

July Jobs Report Shows Unexpected Job Losses

July hiring came in well below expectations, with the economy shedding 23,000 jobs compared with forecasts for an 80,000 gain. Payrolls for May and June were also revised lower by a combined 103,000 jobs. Meanwhile, the unemployment rate edged down from 4.2% to 4.1%.

Bottom line: Some Fed officials cited labor market strength as a reason to support a rate hike at the July meeting. However, the underlying details of this report pointed to a weaker labor market.

Full-time employment declined by 106,000, while part-time employment increased by 138,000. Job losses were elevated in several important areas, including leisure and hospitality (-40,000), retail trade (-19,000), and local government education (-50,000).

Wage growth also came in softer than expected, with average hourly and weekly earnings showing limited gains. While the lower unemployment rate may appear encouraging, the decline was largely driven by a 264,000 drop in the labor force. Since May, the labor force has declined by nearly one million people.

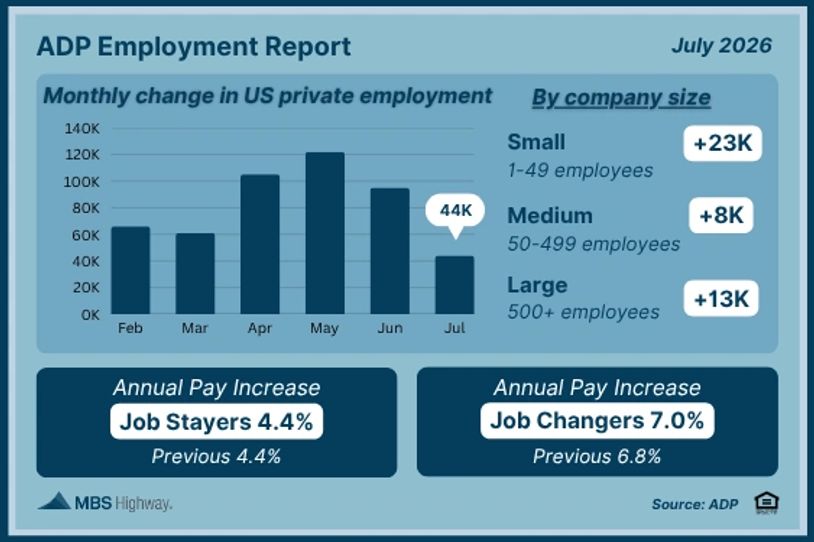

Private Sector Hiring Slows in July

ADP's report reinforced the weaker hiring trend seen in the government's jobs report. Private employers added 44,000 jobs in July, well below expectations of about 70,000. Hiring was led primarily by small businesses, while larger employers added workers at a slower pace. Employees who changed jobs received an average 7% pay increase over the past year, compared with 4.4% for workers who stayed with their current employer.

Bottom line: July hiring was narrowly concentrated rather than broad-based, with education and health services accounting for much of the job growth. Because these sectors are supported by long-term demographic trends, the report doesn't necessarily point to broad strength across the economy.

More Signs the Labor Market is Cooling

The BLS and ADP reports weren’t the only indication of a slowing job market. Job openings fell to 7.36 million in June, slightly below expectations of 7.4 million. The actual number of available jobs may be even lower, as some remote positions are posted in multiple locations.

New unemployment claims remained relatively low at about 199,000, suggesting layoffs are still limited. However, that figure may not tell the full story, as some workers are turning to gig or freelance work instead of filing for unemployment benefits.

At the same time, continuing unemployment claims stayed elevated at 1.8 million, indicating that many unemployed workers are taking longer to find a new job.

The ISM Services Index also showed its employment component falling below 50, signaling contraction, while job site ZipRecruiter described the labor market as subdued in its second quarter earnings report.

Bottom line: Attention now turns to the August jobs report, due in early September, which will be one of the final major labor market reports before the Fed's September 15-16 meeting. Because the Fed balances inflation and the job market when setting policy, this report will be a key input into its next interest rate decision.

What to Watch Ahead

Existing Home Sales kick off the week's economic reports on Tuesday. Attention then turns to inflation, with the Consumer Price Index (CPI) due Wednesday and the Producer Price Index (PPI) on Thursday. The latest weekly jobless claims will be released alongside PPI, providing another snapshot of the labor market. The week wraps up Friday with Retail Sales, a key measure of consumer spending.

Sunset of the week: Murray, Utah